Visualizing the Racial Wealth Gap

Systemic inequities and barriers keep people of color from achieving economic security through employment, education, and homeownership, resulting in racial disparities in wealth and income. These disparities are the consequence of ongoing discrimination, structural inequality, and biases across our institutions. They continue to emerge in new forms of technology — including artificial intelligence and algorithmic risk assessment tools — that influence nearly every facet of life. The confluence of these inequities has created a massive, persistent racial wealth gap in the United States.

Here are three things you should know about the racial wealth gap:

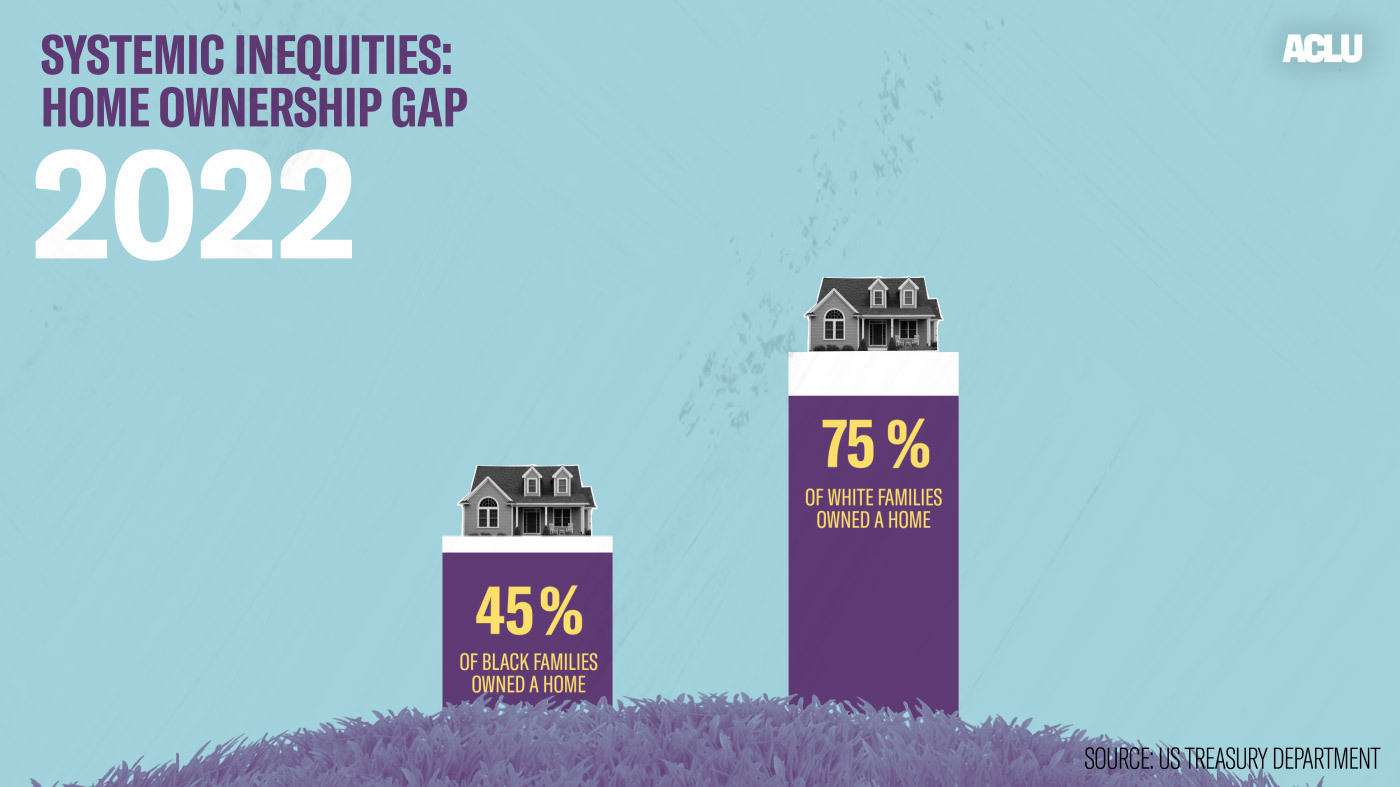

Homeownership

Homeownership has been one of the most effective ways that Americans build wealth, which can be passed down from generation to generation. And although equal access to housing is a civil right, systemic racism within our housing institutions has long kept communities of color from accessing fair housing opportunities. The gap between Black and white families' home ownership has persisted over the years. In 1976, the gap between Black and white families’ home ownership was 25 percent (44 percent of Black families owned a home, compared to 69 percent of white families). In 2022, the gap grew even more to 30 percent (45 percent of Black families owned a home, compared to 75 percent of white families).

Mortgage Loans

When applying for mortgage loans, Black applicants were 1.8 times more likely to be denied for a mortgage than white applicants, while Latino applicants were 1.4 times more likely to be denied than white applicants, according to an analysis of 2019 data. The racial bias in mortgage interest rate is most exemplified by those who earn between $30,000 to $44,999 in annual income, where the median interest rate for Black homeowners is 6.95 percent higher than that of white homeowners.

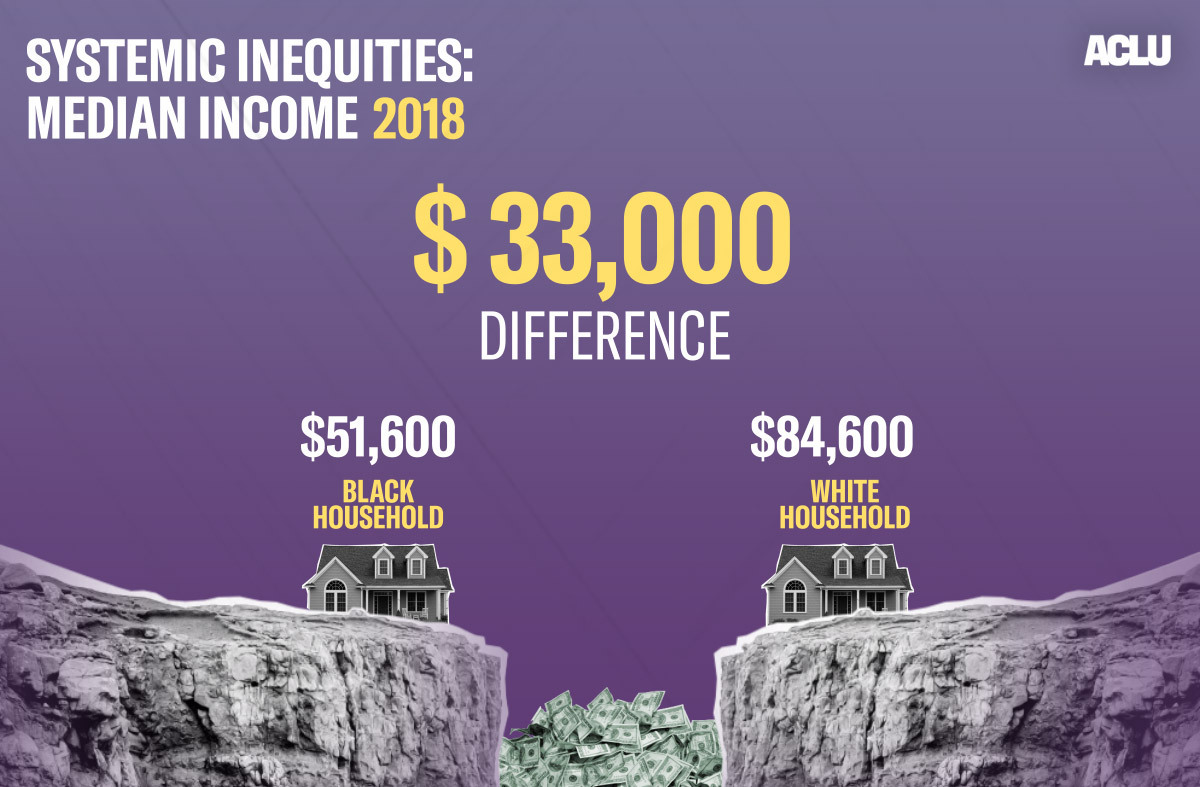

Median Income

The Black-white income gap has persisted and grown since 1970, from a gap of $23,700 in 1970, when the median income for a Black household was $30,400 compared to $54,100 for a white household, to $33,000 in 2018, when the median income for a Black family of three was $51,600 compared to $84,600 for a white family of the same size.

The economic position of Black Americans relative to white Americans over the years remains precarious at best. Through litigation and advocacy, the ACLU works to remedy deeply entrenched sources of inequality and ensure that access to opportunity and the ability to build wealth is available to all. We’ll continue to tackle the roots of the problem by breaking down systems designed to discriminate against Black, Indigenous, and other people of color.

Donate to the ACLU

The ACLU has been at the center of nearly every major civil liberties battle in the U.S. for more than 100 years. This vital work depends on the support of ACLU members in all 50 states and beyond.

We need you with us to keep fighting — donate today.

Contributions to the ACLU are not tax deductible.

Learn More About the Issues on This Page

- Press ReleaseApr 2025

Racial Justice

Federal Court Grants Preliminary Injunction Against Department Of Education’s Unlawful Directive. Explore Press Release.Federal Court Grants Preliminary Injunction Against Department of Education’s Unlawful Directive

CONCORD, N.H. – In a victory for students, parents, and educators, a federal judge has granted a request for a preliminary injunction blocking enforcement of the U.S. Department of Education’s (ED) February 14, 2025, “Dear Colleague” letter against the plaintiffs, their members, and any entity that employs, contracts with, or works with one or more of Plaintiffs or Plaintiffs’ member. The court’s ruling blocks ED’s unprecedented and unlawful attempt to restrict discussions and programs on diversity, equity, and inclusion in educational institutions, and its threat to withhold federal funding for engaging in such efforts. The Dear Colleague Letter’s directive contradicts long-standing legal protections for academic freedom and violates the constitutional rights of students and educators by imposing vague and coercive restrictions on curriculums and programs. The preliminary injunction prevents ED from enforcing the directive while litigation continues, ensuring that schools can continue their educational mission without fear of federal retaliation. “Across the country educators do everything in their power to support every student, ensuring each feels safe, seen, and is prepared for the future. Today’s ruling allows educators and schools to continue to be guided by what’s best for students, not by the threat of illegal restrictions and punishment. The fact is that Donald Trump, Elon Musk, and Linda McMahon are using politically motivated attacks and harmful and vague directives to stifle speech and erase critical lessons to attack public education, as they work to dismantle public schools. This is why educators, parents, and community leaders are organizing, mobilizing, and using every tool available to protect our students and their futures,” said National Education Association President Becky Pringle. “While this interim agreement does not confirm the Department's motives, we believe it should mark the beginning of a permanent withdrawal from the assault on teaching and learning. The Department’s attempt to punish schools for acknowledging diversity, equity and inclusion is not only unconstitutional, but it’s also extremely dangerous -- and functions as a direct misalignment with what we know to be just and future forward. Today’s decision is a critical step toward protecting the freedom to teach, and the freedom to learn,” said Sharif El-Mekki, Center for Black Educator Development CEO & founder. “Today’s ruling is a victory for students, educators, and the fundamental principles of academic freedom. Every student deserves an education that reflects the full diversity of our society, free from political interference,” said Sarah Hinger, deputy director of the ACLU Racial Justice Program. “The federal government has no authority to dictate what schools can and cannot teach to serve its own agenda, and this ruling is an important step in reaffirming that.” Gilles Bissonnette, legal director of the ACLU of New Hampshire, said, “The court's ruling today is a victory for academic freedom, the free speech rights of educators, and for New Hampshire students who have a right to an inclusive education free from censorship. Every student, both in the Granite State and across the country, deserves to feel seen, heard, and connected in school - and that can't happen when classroom censorship laws and policies are allowed to stand." On March 5, the American Civil Liberties Union, the ACLU of New Hampshire, the ACLU of Massachusetts, the National Education Association (NEA), and the National Education Association–New Hampshire, filed a lawsuit in U.S. District Court in New Hampshire, against ED. Also joining the case as plaintiff is the Center for Black Educator Development. Plaintiffs represented in the lawsuit against ED have said they’ve felt like the “Dear Colleague Letter” instigated a “witch hunt” against them. Teachers who have dedicated their lives to helping every student grow to their full potential have been in fear of losing their jobs and teaching licenses if they do not severely restrict what they and their students say and do in their classrooms. The lawsuit challenges ED’s directive on multiple legal grounds. Specifically, the lawsuit argues that ED has overstepped its authority by imposing unfounded and vague legal restrictions that violate due process and the First Amendment; limiting academic freedom and restricting educators’ ability to teach and students’ right to learn; and unlawfully dictating curriculum and educational programs, exceeding its legal mandate. The case will now proceed as the court considers whether to permanently block the Department’s directive. The court’s decision can be found here. A copy of the lawsuit can be found here. - News & CommentaryApr 2025

Racial Justice

Educators Speak Out On Harms Of Unlawful Education Department Directive. Explore News & Commentary.Educators Speak Out on Harms of Unlawful Education Department Directive

The “Dear Colleague Letter” seeks to dictate teaching, curriculum, and school climate, and limit academic free expression. - PodcastApr 2025

Racial Justice

Know Your Right To Transportation Justice With Deborah Archer And Sister Helen Jones. Explore Podcast.Know Your Right To Transportation Justice with Deborah Archer and Sister Helen Jones

- Press ReleaseApr 2025

Racial Justice

Aclu Reacts To Updated Omb Guidance For Ai Use By Federal Agencies. Explore Press Release.ACLU Reacts to Updated OMB Guidance for AI Use by Federal Agencies

WASHINGTON — Today, the Trump administration released updated guidance from the Office of Management and Budget (OMB) on federal agencies' uses of artificial intelligence (AI). The updated guidance reaffirms that American leadership in AI depends on public trust, and emphasizes that AI systems used by the federal government must be safe, fair, and aligned with public interest. “Before using AI to decide who gets a job, mortgage, or federal benefits — and more — federal agencies must first make sure that AI is up to the task, fair, and safe — and discontinue it when it's not,” said Cody Venzke, senior policy counsel with the American Civil Liberties Union. “The new guidance recognizes that American leadership in AI means that AI must make efficient use of taxpayers' resources and work for the American people.” The updated guidance maintains several critical safeguards included in earlier guidance. Federal agencies are still required to perform pre-deployment testing, conduct impact assessments, and discontinue AI that is not sufficiently safe or fair. Ongoing monitoring, remedies and appeals, and human oversight also remain. The guidance covers AI that will affect some of the most critical areas of life like housing, education, employment, and government benefits — which the guidance calls “high-impact AI.” AI is increasingly being used across the federal government to make decisions about our lives, and the updated guidance will help ensure that AI is trustworthy and accountable. AI affects civil rights, civil liberties, and privacy is similarly covered. However, the updated guidance eliminates some key protections that previously supported transparency and civil rights enforcement. Express notice of adverse actions made by AI systems has been removed, weakening transparency for individuals impacted by automated decisions. “Moving forward, the ACLU will continue monitoring the implementation of the guidance and advocating for stronger guardrails where protections have been scaled back or AI poses new harms,” Venzke added. The updated guidance is available here and here.